Fuelling business growth:

When is venture debt the right option?

There are so many funding options available to growing businesses that it can sometimes feel tricky and conflicting, trying to navigate them all.

Most business leaders will have heard of venture capital – it’s the type of business finance that we see frequently on TV, and the idea of raising cash in exchange for a stake in a business is a fairly simple concept to understand.

But what about the other side of the coin: what about venture debt?

What is venture debt?

Venture debt is a type of growth capital, usually provided by specialist lenders to early-stage, but fast-growing businesses that are typically pre-profitability.

Unlike venture capital, which is provided in the form of equity, venture debt is structured in the form of a loan that will be repaid over an agreed term, on an agreed repayment schedule.

The terms “venture loan” or “growth loan” have become a bit of a catch-all, but more traditionally, venture debt is structured as a term loan, alongside an equity kicker component. At Growth Lending for example, we structure our venture debt deals over a 3-5 year term.

Venture debt is typically used to extend a business’ cash runway, enabling the firm to reach its next “event”, whether that be its next equity round, or, in a more mature business, a bridge to profitability.

This type of specialist finance suits businesses with good visibility over revenues, long term contracts and proprietary technology or intellectual property, which is why technology businesses with Software as a Service (SaaS) business models make particularly good candidates.

The history of venture debt

To fully understand venture debt and how it should be used by businesses, it’s helpful to consider the background of the venture debt market and how it has evolved into the product we know today…

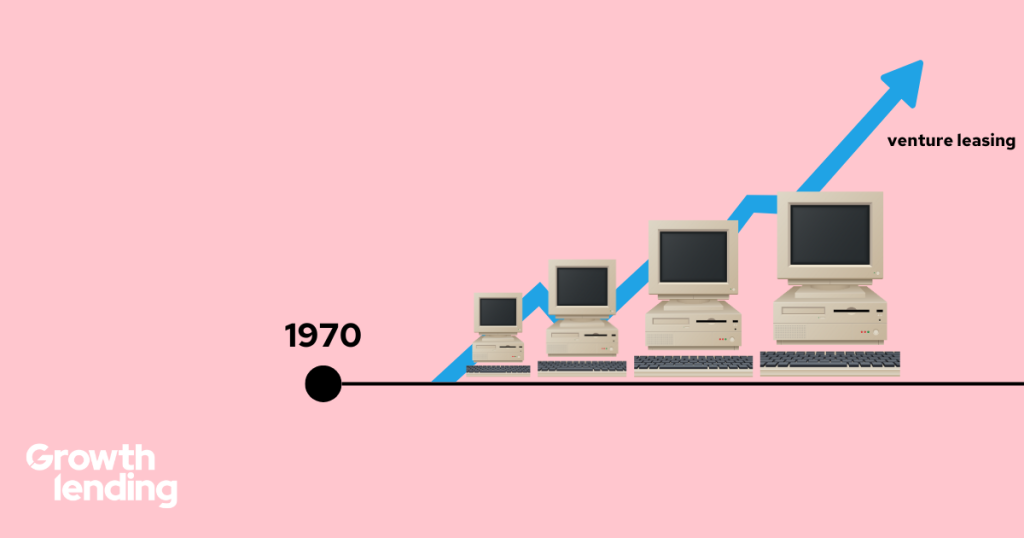

In the 1970s, IT businesses were growing and required cash to purchase hardware and physical assets. They often lacked the cash flow needed to secure funding from traditional sources such as banks, so niche lenders began offering financing for this equipment and the term “venture leasing” was born.

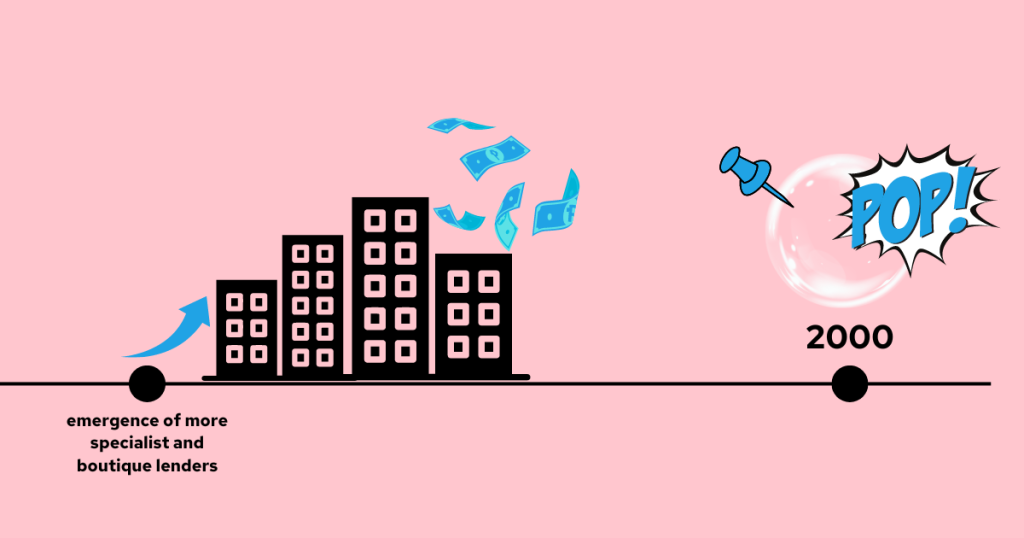

This type of funding existed in various guises until it expanded more widely with the emergence of more specialist and boutique lenders. These lenders would finance the physical assets required by businesses, while venture capital firms would provide an equity injection to fund broader scale-up and growth plans.

Unfortunately, the burst of the dotcom bubble put pay to many of these businesses, and indeed, their funders.

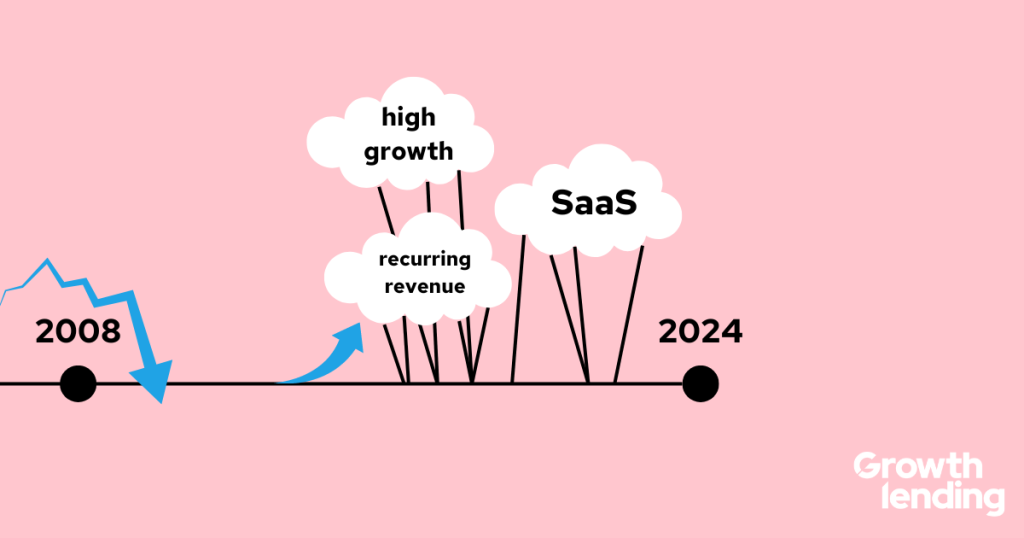

Venture debt then gained traction again following the 2008 financial crisis, when the market as we know it today began to emerge.

Focusing once again on high-growth businesses, often still pre-profitability, venture debt is now underpinned by a SaaS or recurring revenue business model, where substantial capital has already been raised via an equity sponsor or venture capital firm.

What type of business would benefit from venture debt?

Fast-growing, young businesses that have a limited trading history and little, or no, track record of profitability usually struggle to borrow money from conventional sources such as the high street banks, because they do not meet their strict lending criteria.

The consistent rejection can leave business leaders feeling that they have expired all of their options and that their only choice for funding growth is via equity, thus giving up a large chunk of ownership and possibly even ceding control to their investors.

Venture debt however, combines the normal features of a bank loan with the aspects of venture capital that have traditionally been associated with equity finance.

Venture debt providers are as interested in the current and forecasted performance of a business as they are its historical financial performance – a significantly different approach from that of the major banks, which usually require a strong track record and multiple years of financial data before they will lend. These features make venture debt an excellent match for scale-ups and high-growth companies that do not have the positive cash flows that banks require, or the valuable assets that banks expect a borrower to provide as collateral against their debt.

This doesn’t mean that venture debt is suitable for very early stage start-ups that have no track record or significant revenues however, as the business still needs to be able to service the debt. But if you have a proven business model and strong prospects for growth, venture debt could be the perfect tool to help you get there.

When do companies raise venture debt?

When they want to extend cash runway

Typically companies raise venture debt to extend their cash runway until their next “event”. This might be a bridge to profitability, a listing or another equity round. Venture debt provides the business with additional capital to grow, and while this capital does come at a cost, it is a significantly lower cost than the dilution they may face by raising the equivalent via equity at that point in time.

When they already have a proven business model

Here at Growth Lending, we look for businesses that have a proven business model and are generating ARR or revenue of at least £3m, as this gives us confidence in the management team’s abilities thus far.

When they have a clear scale-up plan

Businesses seeking to use venture debt to grow should also have a clear understanding of how they’ll scale their business; the management team should understand the correlation between investment in certain activities and the income that this will likely generate. This relationship between input and output is crucial, as it’s what gives both the business and the lender confidence that the venture debt can be repaid in the future.

Is venture debt really expensive?

Earlier-stage businesses are generally considered higher risk investments, so it would be easy to assume that any kind of loan on offer would be too expensive for an early-stage, pre-profit business to afford.

However, venture debt features a unique facility structure, which is what makes the loan accessible.

It is usually structured as a term loan with an equity kicker on top. This is because a term loan alone, priced to reflect the risk associated with an earlier stage business, would have to encompass an interest rate far too large to be a realistic or attractive option. By introducing an equity kicker, which gives the lender the opportunity to benefit from the upside of the investment, the lender is able to offer an interest rate on the term loan that is more affordable.

How to use venture debt to grow your business

Venture debt is a form of growth capital, so it is usually used to support activities that underpin a business’ growth.

These initiatives could include:

- Extending cash runway to reach the next inflection point, whether that’s the next equity round or reaching profitability

- Funding M&A activity – buy and builds, or platform acquisition strategies can be powerful growth strategies businesses

- Providing working capital – this can be particularly helpful for businesses that might experience seasonality in their business cycles

- Supporting capital expenditure

The common factor however, is that the management team must have a strong grasp on what they will be using the funding for and have confidence that these growth strategies will deliver.

Find out more about how a business can use growth capital to grow, here.

What comes next if I want to raise venture debt?

If you believe that your business could be a good fit for venture debt, the next step is to speak to an expert. This could be an advisor, or a lender, but they should be very clear from the outset about whether their services are a good match for your business’ needs.

If you’d like further information, or guidance on the next steps of your growth journey, and are not sure who to speak to, reach out to a member of our lending team who will be more than happy to help.